When you walk into a bank to get a mortgage, they ask for your credit score, pay stubs, and bank statements. In DeFi, none of that matters. All they ask is: how much crypto do you have? That’s where collateral factor and borrowing power come in - two simple but powerful concepts that are changing how money moves in the digital age.

What Is a Collateral Factor?

The collateral factor is just a percentage. It tells you how much of your crypto you can borrow against. If a platform says the collateral factor for ETH is 70%, that means for every $1,000 worth of ETH you lock up, you can borrow up to $700. It’s not magic - it’s math. And it’s built into every DeFi lending protocol like Aave, Compound, and MakerDAO.Why not 100%? Because crypto prices swing. ETH might be worth $3,200 today and $2,800 tomorrow. If lenders let you borrow 100% of your asset’s value, a small dip could leave them with nothing if you default. So platforms assign lower factors to risky assets. Bitcoin (BTC) might have a 75% factor. Stablecoins like USDC? Often 85% or higher. Why? Because they’re designed to stay at $1. Less risk = higher borrowing power.

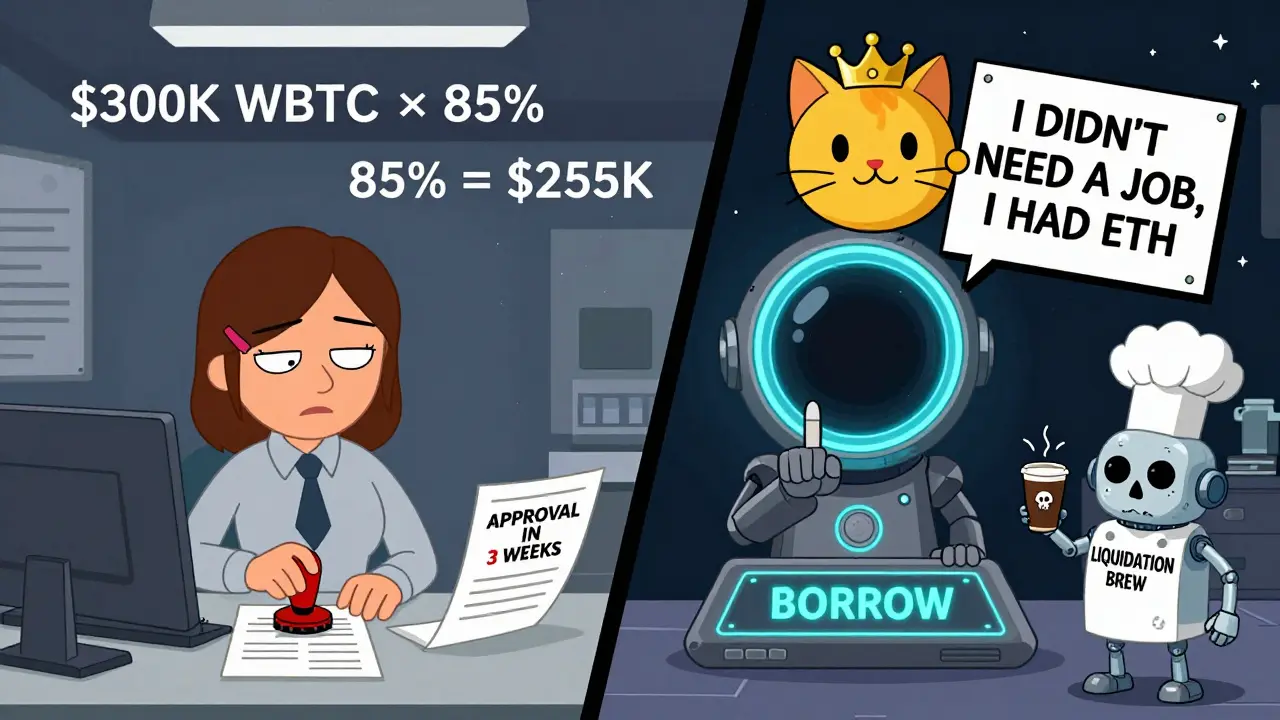

Here’s how it works in real life. Say you deposit 5 WBTC. Each WBTC is worth $60,000. Total value: $300,000. If WBTC has an 85% collateral factor (as Compound lists), your borrowing power is $300,000 × 0.85 = $255,000. You can now borrow any asset on that platform - USDC, DAI, even ETH - up to that amount.

What Is Borrowing Power?

Borrowing power is the total amount you’re allowed to borrow. It’s not fixed. It changes every time the price of your collateral moves. If ETH drops 20%, your borrowing power drops too. If you’ve already borrowed close to your limit, you could get liquidated.In traditional finance, borrowing power depends on your credit history, income, debt-to-income ratio, and how long you’ve had a bank account. It can take years to build. In DeFi? You get borrowing power the second you connect your wallet and deposit crypto. No background check. No employment verification. Just crypto in, cash out.

But here’s the catch: your borrowing power isn’t just about one asset. Most platforms let you deposit multiple assets. Say you put in $10,000 in USDC (85% factor), $5,000 in ETH (70% factor), and $2,000 in SOL (50% factor). Your total borrowing power is:

- USDC: $10,000 × 0.85 = $8,500

- ETH: $5,000 × 0.70 = $3,500

- SOL: $2,000 × 0.50 = $1,000

Total: $13,000. That’s your borrowing power. Add more collateral? It goes up. Sell some? It goes down.

DeFi vs. Traditional Lending: A Direct Comparison

Traditional banks and DeFi protocols both use collateral. But how they treat it is totally different.

| Aspect | DeFi Lending | Traditional Lending |

|---|---|---|

| Collateral Type | Any crypto asset (ETH, BTC, USDC, etc.) | Real estate, vehicles, or cash deposits |

| Collateral Factor | Dynamic, set by protocol based on volatility and liquidity | Fixed, based on asset class (e.g., 80% LTV for homes) |

| Borrowing Power Calculation | Sum of (asset value × collateral factor) across all deposited assets | Based on credit score, income, debt-to-income ratio |

| Approval Time | Instant (smart contract interaction) | Days to weeks (paperwork, underwriting) |

| Risk Management | Automatic liquidation if collateral ratio falls below threshold | Foreclosure process (legal, slow, expensive) |

| Credit Check | None | Required |

Traditional lenders care about your history. Did you pay your credit card on time? Do you have a steady job? DeFi doesn’t care. It only cares about your collateral. That’s why someone with no credit score in the U.S. can still borrow $50,000 in DeFi - if they have enough crypto.

Why Collateral Factors Change

Collateral factors aren’t set in stone. They shift with the market. If a token gets hacked, or if its trading volume drops, the protocol will lower its factor. For example, when the LUNA crash happened in May 2022, protocols like Aave dropped the collateral factor for LUNA to 0% overnight. No one could borrow against it anymore.

On the flip side, when a new asset becomes popular - like a newly launched Layer 2 token - protocols might test it with a low factor first (say, 40%). If it holds value and trades heavily over weeks, they might raise it to 60% or 70%. It’s all about risk.

Platforms like Compound and Aave publish their collateral factors publicly. You can check them before you deposit. Always do. A 5% drop in collateral factor can mean a 10% drop in your borrowing power - and that’s enough to trigger a liquidation if you’re already near your limit.

How Liquidations Work (And How to Avoid Them)

Here’s the scariest part of DeFi: if your collateral value drops too much, your loan gets sold automatically.

Every protocol has a liquidation threshold. For example, if you borrow $10,000 and your collateral value is $15,000, your loan-to-value (LTV) is 67%. The protocol might set the liquidation threshold at 80%. That means if your collateral drops to $12,500 (because the price fell), your LTV hits 80% - and the bot starts selling your assets to repay the loan.

You don’t get a warning. No phone call. No letter. Just a blockchain transaction that drains your position. That’s why monitoring your collateral ratio isn’t optional - it’s survival.

Smart users set alerts. They keep extra collateral on hand. They avoid borrowing the full limit. If you’re borrowing $75,000 against $100,000 in collateral (75% LTV), you’ve got almost no buffer. A 10% market dip could liquidate you. Aim for 50% LTV or lower if you want to sleep at night.

Why This Matters for Everyday Users

DeFi isn’t just for traders. It’s for anyone who needs cash fast - and doesn’t want to wait weeks for a bank.

Imagine you’re a freelancer in Colorado. You get paid in ETH. You need $8,000 for a car down payment. You don’t have a credit card. You can’t get a personal loan. But you have 3 ETH worth $12,000. With a 70% collateral factor, you borrow $8,400 in USDC. You pay for the car. You hold your ETH. If ETH goes up, you’re ahead. If it drops, you top up your collateral or pay back the loan.

Or say you’re a student in Texas. You’ve been saving Bitcoin for two years. You need $3,000 for tuition. You don’t want to sell your BTC - you think it’ll double. So you use it as collateral. You borrow $2,250 (at 75% factor). You pay tuition. You keep your BTC. You’re not selling your future. You’re using it as a tool.

This isn’t theory. It’s happening every day. In 2025, over $12 billion in crypto was locked as collateral across DeFi protocols. Millions of people are using it to access liquidity without giving up their assets.

What’s Next?

Traditional banks are watching. Some are testing crypto-backed loans. JPMorgan has filed patents for blockchain-based lending. Fidelity offers crypto custody and is exploring lending products. The line between DeFi and traditional finance is blurring.

Future protocols will use real-time data - not just price, but trading volume, on-chain activity, even social sentiment - to adjust collateral factors. Some are testing cross-chain collateral: using Solana tokens to borrow on Ethereum. Others are building insurance layers to protect against sudden drops.

One thing’s clear: the old system of credit scores and paperwork is being replaced by a system of code, collateral, and clear rules. You don’t need a bank to trust you. You just need to prove you have something valuable.

Key Takeaways

- Collateral factor = the percentage of your crypto you can borrow against (e.g., 70% means $700 for every $1,000 you deposit).

- Borrowing power = the total amount you can borrow, based on all your collateral and their individual factors.

- Stablecoins (USDC, DAI) have higher factors than volatile assets (SOL, ADA) because they’re less risky.

- DeFi gives instant borrowing power - no credit check, no paperwork.

- Automatic liquidations are real. Always keep your loan-to-value below 70% to stay safe.

- Collateral factors change. Monitor them. If a token’s factor drops, your borrowing power drops too.

Can I borrow more than my collateral is worth?

No. You can only borrow up to your borrowing power, which is calculated as the sum of each asset’s value multiplied by its collateral factor. Even if you deposit $100,000 in ETH with a 70% factor, your max borrow is $70,000 - not $100,000. You can’t borrow 100% of your collateral, and you definitely can’t borrow more.

Do I need to repay the loan in the same asset I borrowed?

No. You can deposit ETH and borrow USDC. Or deposit BTC and borrow DAI. You repay in the asset you borrowed - so if you borrowed USDC, you repay in USDC. The protocol doesn’t care what you deposited - only what you borrowed and what you have as collateral.

What happens if I don’t repay the loan?

If you don’t repay and your collateral ratio falls below the liquidation threshold, your collateral gets automatically sold to cover the debt. You lose your assets. There’s no grace period. No negotiation. The smart contract executes the liquidation without human input. It’s not optional - it’s built into the system.

Can I use my home as collateral in DeFi?

Not directly. DeFi protocols only accept crypto assets. But some companies are building bridges - like tokenizing real estate and turning it into a crypto asset that can be used as collateral. These are still early, and often require third-party services. For now, if you want to use your home, you still need a traditional mortgage.

Is DeFi lending safer than a bank loan?

It’s different. DeFi eliminates credit checks and paperwork, but introduces new risks: price volatility, smart contract bugs, and automatic liquidations. Banks are slower and more regulated, but they offer consumer protections like forbearance and loan modifications. Neither is universally safer - it depends on your risk tolerance and how carefully you manage your position.