Imagine you put your hard-earned crypto into a liquidity pool, expecting to earn a steady stream of trading fees. A few weeks later, you check your balance and realize that if you had just left your coins in a cold wallet, you'd actually have more money. This frustrating gap is known as Impermanent Loss is a temporary reduction in the value of deposited assets in an automated market maker compared to simply holding them, caused by price divergence between the paired assets. It is the single biggest risk for anyone acting as a liquidity provider in DeFi. But here is the catch: not all pools are created equal. Depending on the mathematical formula the platform uses, your risk of losing money to price swings can vary from "nearly zero" to "absolutely brutal."

The Basics: Why Does This Happen?

At its core, impermanent loss is an opportunity cost. When the price of an asset you've deposited changes, the Automated Market Maker (AMM) must adjust the ratio of assets in the pool to keep the price accurate for traders. Arbitrageurs swoop in to buy the cheaper asset and sell the more expensive one until the pool price matches the market price. This means the AMM effectively sells your winning asset as it goes up and buys more of the losing asset as it goes down.

The loss is called "impermanent" because if the assets return to the exact price ratio they had when you deposited them, the loss disappears. It only becomes permanent the moment you withdraw your funds. For many, the goal is to earn enough in trading fees to offset this divergence. However, during extreme volatility, the loss can easily outpace the fees, leaving you with less than you started with.

Constant Product AMMs: The Standard Risk

Most people are familiar with the constant product formula (x × y = k), used by platforms like Uniswap V2, SushiSwap, and PancakeSwap. In these pools, the product of the two asset quantities must remain constant. This creates a hyperbolic price curve that makes impermanent loss mathematically inevitable for uncorrelated assets.

To put some numbers on this, a 50% increase in the price of one asset leads to a 1.26% loss. If the price doubles (100% increase), you're looking at a 5.72% loss. If the asset moons and jumps 300%, your impermanent loss hits 20%. For these "classic" AMMs, the vulnerability is high because the pool doesn't care about the actual market price; it just reacts to the trades coming in.

StableSwap: Minimizing Loss with Correlation

Not every pool needs to handle volatile assets. Curve Finance realized that if you're pairing two stablecoins (like USDC and USDT), they should essentially always be the same price. They developed the StableSwap invariant, which blends a constant sum formula with a constant product formula.

This design keeps the price curve very flat near the $1 peg. Because the assets are highly correlated, the price divergence is minimal. In practice, impermanent loss in these pools often stays below 0.1% as long as the price difference remains under 10%. It is a much safer bet for risk-averse providers, though the rewards are typically lower because the risk is significantly reduced.

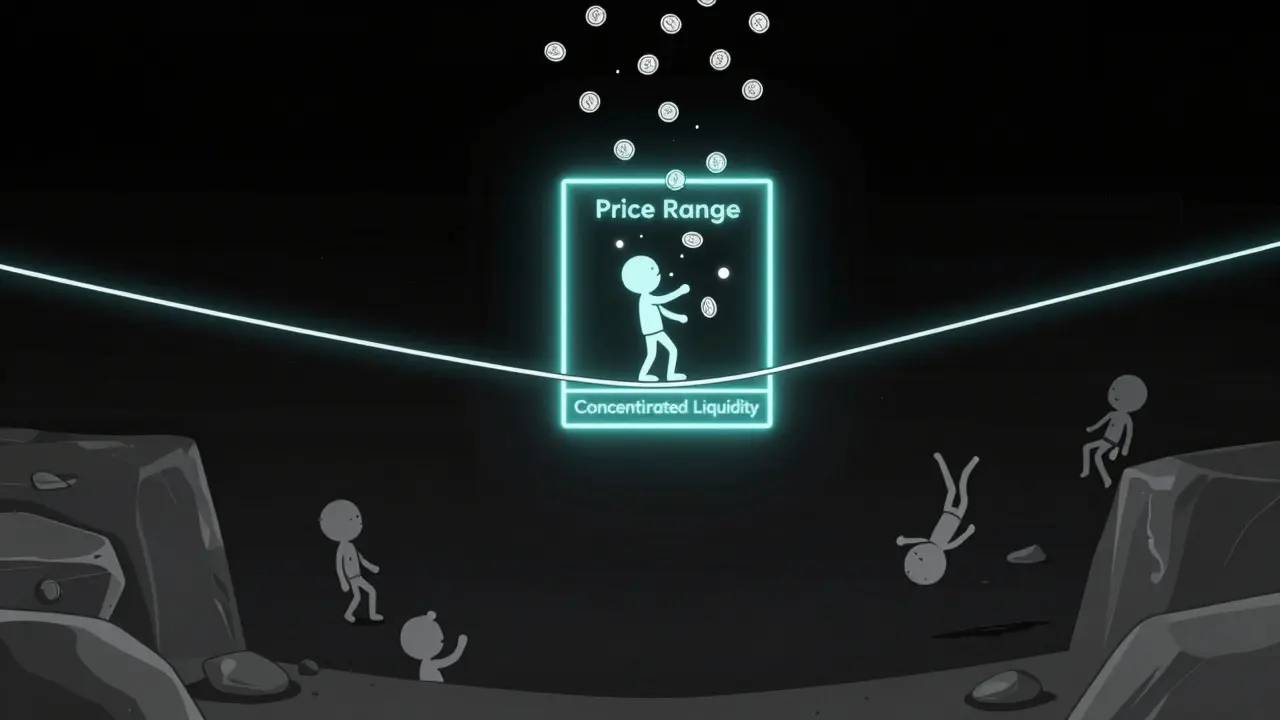

Concentrated Liquidity: High Reward, High Stakes

With the launch of Uniswap V3, the game changed. Instead of providing liquidity across the entire price range from zero to infinity, providers can pick a specific "price range." This is called concentrated liquidity. If the market price stays within your chosen range, you earn massive fees because your capital is working much harder.

However, this is a double-edged sword. While a well-managed position can reduce the impact of impermanent loss by 30-70%, a mistake in your range can lead to disaster. If the price moves outside your range, your position is converted entirely into the less valuable asset and stops earning fees. During the ETH crash of March 2023, some misconfigured V3 positions suffered losses as high as 67.2%, while V2 providers only lost about 20% in the same window.

| AMM Type | Example Protocol | Avg. Impermanent Loss | Management Effort |

|---|---|---|---|

| Constant Product | Uniswap V2 | 8.7% | Low (Passive) |

| StableSwap | Curve Finance | 0.3% | Low (Passive) |

| Concentrated Liquidity | Uniswap V3 | 3.1% (Optimal) | High (Active) |

| Weighted Pools | Balancer | 4.2% - 15.8% | Medium |

Weighted Pools and Proactive Market Makers

Other designs try to tackle the problem from different angles. Balancer allows for weighted pools (like 80/20 instead of 50/50). This changes the loss curve; for instance, an 80/20 pool might experience a 12.36% loss during a 2x price change, compared to 5.72% in a 50/50 pool. It gives providers more flexibility in how much exposure they want to a specific asset.

Then there are the "smarter" AMMs. DODO uses a Proactive Market Maker (PMM) algorithm that relies on external oracles to set prices. Theoretically, this could eliminate impermanent loss entirely because the pool doesn't rely on arbitrageurs to move the price. However, it introduces a new risk: oracle failure. If the price feed lags or gets hacked, the loss can return in the form of "residual loss," which has been seen as high as 3.8% during technical glitches.

Strategies to Protect Your Capital

You don't have to just cross your fingers and hope for the best. Experienced liquidity providers use a few specific heuristics to stay in the green:

- Stick to Correlated Assets: Pairing two assets that move together (like wrapped BTC and BTC) almost entirely removes the risk of impermanent loss.

- Check the Fee-to-Loss Ratio: If a pool has a high trading volume and generates 40% annualized yield, it can easily cover a 5-10% divergence loss.

- Use Range Tools: If you're using Uniswap V3, don't guess. Tools like Zapper or Risk Harbor can help you simulate ranges to see where your "break-even" point is.

- Avoid Low-Liquidity Pairs: In pools with very little TVL, a single large trade can cause a massive price swing, triggering instant impermanent loss before you can react.

The Future: Hybrid Models and Oracle Integration

The industry is moving toward a world where liquidity providers aren't just "cannon fodder" for arbitrageurs. New proposals, like Uniswap V4's dynamic fee tiers and hooks, aim to let pools adjust fees in real-time based on volatility. If the market gets crazy, fees go up, helping providers cover the increased impermanent loss.

We are also seeing a shift toward hybrid models that use multi-oracle redundancy to keep pool prices pegged to the real world without the lag. The goal is to bring the residual loss down to under 1%, making DeFi liquidity attractive to institutional investors who can't afford a 20% hit to their principal just because of a price swing.

Is impermanent loss always a bad thing?

Not necessarily. It's a relative loss compared to holding. If the assets in your pool increase significantly in value, you still make a profit in absolute terms; you just make less than you would have if you'd just held the coins. When you add the trading fees earned, you can often end up with more total value than a simple HODL strategy.

Can I completely avoid impermanent loss?

Yes, in a few ways. First, provide liquidity to stablecoin-only pools (like those on Curve), where assets are pegged to the same value. Second, use single-sided liquidity models like those attempted by Bancor, though these often carry other risks like oracle reliance. Third, pair highly correlated assets that move in lockstep.

Which is riskier: Uniswap V2 or V3?

Uniswap V3 is riskier for beginners because it requires active management. If you set a narrow price range and the market moves past it, you can suffer much steeper losses than in V2. However, for pro traders, V3 is more efficient because it allows them to hedge their positions and earn higher fees to offset the loss.

How do I calculate my potential loss?

For standard 50/50 pools, the formula is (2 * square root of price ratio) / (1 + price ratio) - 1. Since that's a headache to do by hand, most providers use real-time calculators like Zapper or specialized DeFi spreadsheets to estimate loss based on a predicted price change (e.g., a 2x price move equals a 5.72% loss).

Does the amount of liquidity I provide affect the percentage of loss?

No. Impermanent loss is a percentage of the total value. Whether you provide $100 or $1,000,000, a 2x price divergence in a constant product pool will result in the same 5.72% loss relative to holding. However, the absolute dollar amount of the loss will be higher if you provide more capital.

Next Steps for Liquidity Providers

If you are just starting out, avoid volatile pairs. Start with a stablecoin pool to understand how fees are earned without stressing over price swings. Once you're comfortable, move to a 50/50 volatile pair in a V2-style pool. Only jump into concentrated liquidity (V3) after you have spent a few dozen hours simulating ranges and understanding how to "rebalance" your position when the market moves. Remember, the key to winning in DeFi is not just chasing high APY, but managing the divergence loss that comes with it.

JERRY ORTEGA

been through this myself and yeah it really sucks when you see that gap but just keep it simple and stick to stables if you are new to the game