Imagine sending a single euro from one crypto wallet to another. In most parts of the world, that tiny transaction flies under the radar. But in the European Union, that same transfer triggers a massive compliance check. This is the reality of the Travel Rule compliance era we entered fully on December 30, 2024. The EU has implemented a strict "zero threshold" policy, meaning there is no minimum amount below which you can skip sharing data. If you are running a crypto business here, this isn't just red tape; it's the new operating system.

The shift wasn't sudden. It was built on years of legislative groundwork, culminating in two major regulations: Regulation (EU) 2023/1113 and Regulation (EU) 2023/1114, known as MiCA. While the laws passed in mid-2023, regulators gave Crypto Asset Service Providers (CASPs) an 18-month grace period to get their houses in order. That clock ran out at the end of 2024. Now, every transfer between registered entities requires full transparency. No exceptions. No small amounts ignored.

The Core of the Zero Threshold Policy

To understand why this matters, you have to look at how the EU differs from the rest of the world. The Financial Action Task Force (FATF), the global body that sets anti-money laundering standards, originally suggested a threshold of $1,000 or €1,000 for crypto transactions. Many countries followed suit. The United States, for instance, still uses a $3,000 threshold. Under those rules, if I send you $500, neither our exchanges need to swap personal details.

The EU decided that approach left too much room for abuse. Their logic? Criminals don't just move millions in one go; they break funds into smaller chunks to avoid detection-a technique called structuring. By setting the threshold to €0, the EU closes that loophole completely. Every time money moves between two CASPs within the bloc, the sender’s identity and the receiver’s identity must travel with the funds.

This creates a chain of custody for digital assets that mirrors traditional banking. When you wire cash via SWIFT, your bank knows who you are and where the money is going. The Travel Rule aims to bring that same level of visibility to blockchain networks, which were previously designed for pseudonymity. For legitimate businesses, this builds trust. For illicit actors, it raises the cost and risk of operating in Europe significantly.

| Jurisdiction | Threshold Amount | Implementation Status |

|---|---|---|

| European Union | €0 (Zero) | Active since Dec 30, 2024 |

| United States | $3,000 | Active (FinCEN guidance) |

| FATF Recommendation | $1,000 / €1,000 | Global Standard |

| France (Pre-EU Reg) | €0 | Early adopter precedent |

What CASPs Must Do Right Now

If you operate as a Crypto Asset Service Provider (CASP)-whether you're an exchange, a wallet provider, or a broker-your responsibilities have shifted dramatically. You are no longer just processing transactions; you are verifying them. The regulation places specific burdens on both the originating CASP (the sender's side) and the beneficiary CASP (the receiver's side).

As the originating entity, you must collect accurate information about the originator before the transaction leaves your platform. This includes their name, address, account number, and national identification number. You then need to transmit this data securely to the receiving CASP. It’s not enough to hope the other guy checks it; you have to push the data through compliant channels.

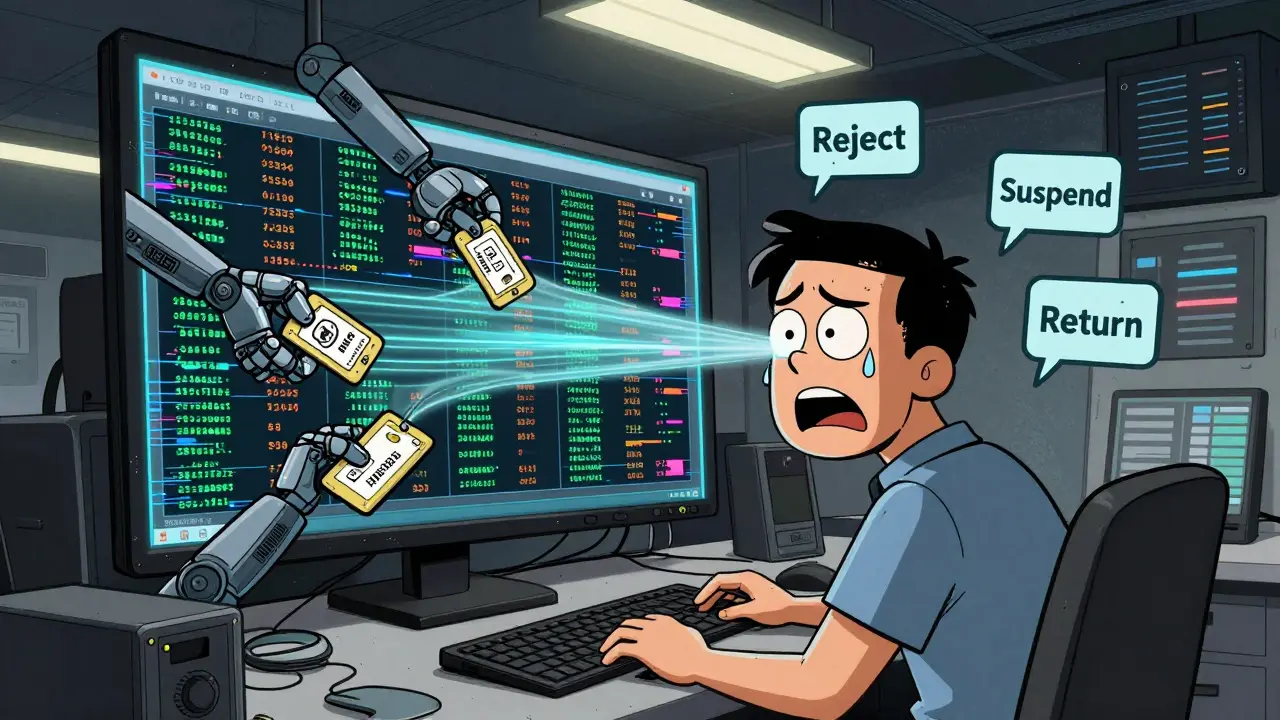

On the receiving end, things get trickier. What happens when a transaction arrives without the required data? The EU doesn't let you just ignore it. Beneficiary CASPs must have effective procedures to identify missing information. You have discretionary authority here, but it comes with risk. You can choose to:

- Reject the transaction: Send it back immediately if the risk is high.

- Suspend the transaction: Hold the funds while you try to gather the missing info.

- Return the transaction: Reverse the transfer if you can't verify the source.

- Execute the transaction: Only if you’ve assessed the risk and deemed it acceptable (which is rare under a zero-threshold regime).

This decision-making process needs to be documented. If you repeatedly accept transactions from counterparties who fail to provide data, you’re breaking the law. The regulation demands a proactive, risk-based approach. You can’t just be passive. You have to actively police the flow of information.

The Technical Challenge: Scaling Compliance

The biggest headache for most CASPs isn't the legal theory; it's the engineering. Handling thousands of transactions per second is hard. Doing it while attaching verified personal data to each one is exponentially harder. You can't just email PDFs back and forth. You need automated, real-time systems.

Compliant solutions must scale without causing service interruptions. If your compliance check takes five minutes, your users will leave. If it fails, you face fines. This has spawned a whole industry of Travel Rule technology providers. Companies like KYCAID and others have built platforms specifically to handle this data exchange. These tools do several critical jobs:

- Counterparty Verification: They instantly check if the receiving CASP is registered and compliant.

- Data Formatting: They ensure the information matches the exact schema required by EU regulators.

- Secure Transmission: They use encrypted messaging protocols to send data directly between institutions, bypassing public blockchain limitations.

- AML Screening: They cross-reference names against sanctions lists and watchlists in real-time.

Integration is key. You need these systems to plug into your existing infrastructure seamlessly. If you’re building a new platform, bake this in from day one. If you’re legacy, you’re likely facing a costly retrofit. The goal is minimal disruption to the user experience. Ideally, the customer shouldn't even notice the compliance happening behind the scenes.

Cross-Border Headaches: The Sunrise Issue

Domestic transfers within the EU are manageable because everyone is playing by the same rules. The real pain point emerges when you deal with jurisdictions outside the bloc. This is often called the "Sunrise Issue." Imagine you receive a transfer from an exchange in a country that hasn't implemented the Travel Rule, or one that uses a different standard.

The European Banking Authority (EBA) flags these scenarios as high-risk for money laundering and terrorism financing. When data is missing from an international transfer, you can't just assume it's safe. You have to dig deeper. This might mean enhanced due diligence (EDD). You may need to request additional documentation from the user, such as proof of income or source of funds.

If the foreign counterparty consistently fails to provide data, you may have to terminate the business relationship entirely. It’s a harsh reality, but necessary. The EU won't allow its financial system to be used as a blind spot for global illicit flows. This creates a competitive advantage for EU-compliant firms but isolates those who refuse to adapt.

Risks of Non-Compliance

Let’s be clear about the stakes. Ignoring the Travel Rule isn't a minor oversight. It’s a direct violation of EU law. The consequences fall into three buckets:

Regulatory Sanctions: Fines can be substantial. Depending on the member state, penalties can reach millions of euros or a percentage of your annual turnover. Repeat offenders face stricter scrutiny and potential license revocation.

Reputational Damage: In the crypto world, trust is currency. If your platform is known for lax compliance, institutional investors will stay away. Banks will cut off your fiat rails. You become a pariah in the regulated space.

Operational Exclusion: Other compliant CASPs will stop doing business with you. If you can't prove you’re following the rules, no one else will send you money. You effectively lock yourself out of the market.

The zero-threshold model leaves no room for "good faith" errors. You either have the data, or you don't. And if you don't, you have to act.

Looking Ahead: Harmonization and Evolution

As we move further into 2026, the focus is shifting from basic implementation to refinement. Regulators are watching how these systems perform. Are there bottlenecks? Is data privacy being respected? The EU General Data Protection Regulation (GDPR) intersects heavily with the Travel Rule. You’re collecting sensitive personal data, so you must protect it fiercely.

We expect to see more harmonization of cross-border procedures. The EU is pushing for global adoption of similar standards. If other regions follow the zero-threshold lead, the current fragmentation will ease. Until then, CASPs must maintain sophisticated jurisdictional awareness engines to navigate the patchwork of global rules.

For now, the message is simple: Adapt or exit. The era of anonymous micro-transactions in regulated EU crypto markets is over. The infrastructure is live, the thresholds are gone, and the eyes of the regulators are open.

What exactly is the "zero threshold" in the EU Travel Rule?

The zero threshold means there is no minimum transaction value exempt from compliance. Unlike the US $3,000 limit, every crypto transfer between CASPs in the EU, even for €1, requires the exchange of originator and beneficiary information.

When did the EU Travel Rule become fully active?

The regulation became fully operational on December 30, 2024, after an 18-month grace period that allowed CASPs to build their compliance frameworks following the initial approval in 2023.

Who does the Travel Rule apply to?

It applies to all Crypto Asset Service Providers (CASPs) registered in the EU, including exchanges, wallet providers, and brokers. It covers transactions between these entities, not necessarily peer-to-peer transfers between private individuals.

What should a CASP do if incoming transaction data is missing?

Beneficiary CASPs must assess the risk. They can reject, return, or suspend the transaction. Executing the transaction is only permissible if the risk is deemed low, which is difficult to justify under a zero-threshold regime without proper verification.

How does the EU rule compare to the US approach?

The EU is stricter. The US uses a $3,000 threshold, meaning smaller transactions don't require data exchange. The EU's €0 threshold makes it the most stringent jurisdiction globally, aiming to prevent structuring and enhance total transparency.